{kind=link}

Officers approaching retirement often face a critical financial dilemma: should they opt for pension commutation? This article seeks to provide clarity on this important choice.

The short and unequivocal answer is yes – you should commute your pension.

This recommendation holds good despite a fundamental flaw in the formula used to compute the Commuted Value of Pension (CVP) for government servants retiring on or after 2 September 2008. While post-2008 retirees receive a lower commuted amount compared to those who retired earlier – owing to the revised Commutation Table – and also pay higher interest, commutation continues to offer substantial financial advantages.

It is noteworthy that the revised table is based on an expired Mortality Table of the Life Insurance Corporation of India (LIC), rendering it legally and actuarially questionable. Yet, even under these unfavourable and flawed assumptions, pension commutation remains a financially prudent option for most retirees.

What is Commutation of Pension?

Commutation of pension is a statutory facility that allows a Government servant to convert a portion of the monthly pension into a one-time lump sum payment, called the Commuted Value of Pension (CVP), at the time of retirement or thereafter. The legal framework governing this facility is contained in the Central Civil Services (Commutation of Pension) Rules, 1981.

Under Rule 4, a pensioner is entitled to commute up to 40% of the basic pension. If the application for commutation is submitted within one year of retirement, no medical examination is required (Rule 6). Applications made after one year require medical examination. The commuted value is calculated in accordance with Rule 10, based on the age next birthday of the pensioner and the notified commutation table.

Upon payment of the commuted value, the monthly pension is reduced by the commuted portion as per Rule 11. However, this reduction affects only the pension actually drawn, not the basic pension sanctioned.

Importantly, Dearness Relief (DR) continues to be payable on the full basic pension originally sanctioned, including the commuted portion. Commutation does not reduce the basic pension for the purpose of DR calculation. The commuted portion of pension is restored after 15 years from the date of commutation.

In essence, commutation represents an advance payment of a part of pension, without affecting entitlement to Dearness Relief and with full restoration after a defined period, making it a significant financial decision for retiring Government servants.

Understanding Pension Commutation

The Commuted Value of Pension (CVP) is calculated using a Commutation Factor (CF) linked to the retiree’s age at the time of retirement. This factor is derived from the Commutation Table, which in turn is actuarially constructed from mortality data supplied by LIC through what is known as a Mortality Table.

Mortality Tables are prepared under the supervision of the Insurance Regulatory and Development Authority of India (IRDAI) and are published by the Institute of Actuaries of India (IAI). The IAI analyses demographic and longevity data to determine actuarial values, which form the basis for insurance premiums and pension commutation factors.

Impact of the Revised Commutation Table

Commutation Table-1 was in force from 1 March 1971 to 1 September 2008. It was replaced by Commutation Table-2, applicable to government servants retiring on or after 2 September 2008.

The formula for calculating CVP is: P × 40% × CF × 12 where P represents the full sanctioned pension.

Under Table-1, the commutation factor for retirement at age 60 was 9.81. Table-2 reduced this factor sharply to 8.194, representing a 16.5% reduction: (9.81–8.194) × 100/9.81 = 16.5%

This reduction directly translates into a corresponding decrease in the commuted amount payable to post-September 2008 retirees.

Additionally, the implicit rate of interest charged on commutation increased from 4.75% to 8% per annum. Despite these adverse changes, officers whose effective income-tax rate exceeds 16.67% still derive a clear financial benefit from commutation, even though recovery continues for 15 years.

Is the 15-Year Recovery Period Justified?

A common concern among retirees is whether the 15-year recovery period is fair or financially justified.

Detailed calculations show that even after completing the full recovery period, pensioners in higher tax slabs remain net gainers. Only when the effective tax rate (after exemptions and deductions) falls below 16.67% does the present value of the pension foregone exceed the commuted amount received upfront.

In such limited cases alone would there be a theoretical financial argument for shortening the recovery period. Consequently:

- Pensioners with effective tax rates above 16.67% benefit from commutation, even with the full 15-year recovery.

- Those below this threshold are financially disadvantaged.

For analytical clarity, the commuted amount may be viewed as a loan received upfront, with the pension foregone (without TDS) representing the instalment repayments. Under this framework, the 15-year recovery period corresponds to the loan tenure.

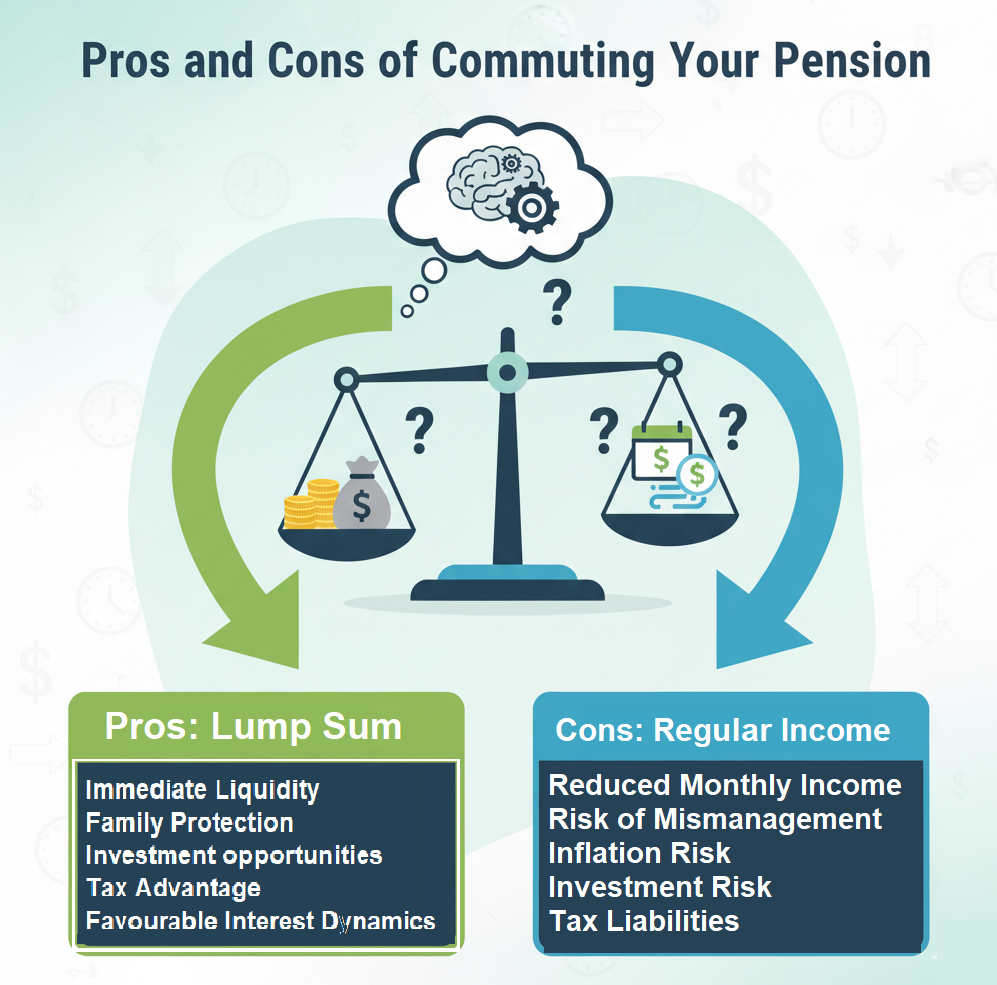

Why You Should Opt for Pension Commutation?

The case for commutation is compelling for the following reasons:

- Immediate Liquidity

Commutation provides a substantial tax-free lump sum at retirement, which can be utilised for emergencies, investments, debt repayment, or other personal priorities. Since commutation is a one-time exercise, the monthly deduction remains fixed, while the pension continues to rise due to Dearness Relief and Pay Commission revisions, making the deduction progressively less burdensome.

- Family Protection

In the unfortunate event of the pensioner’s demise, commutation recoveries stop immediately, and the family receives the full pension. If commutation is not exercised, the family permanently loses the opportunity to receive the lump sum – resulting in a significant financial disadvantage.

- Investment Opportunities

If the lump sum is not immediately required, it may be invested in safe instruments such as bank fixed deposits, the Senior Citizens Savings Scheme (SCSS), or the Post Office Monthly Income Scheme (POMIS). Where appropriate, the amount can also be transferred to the spouse’s account as an interest-free loan (if the spouse has no independent income), thereby optimising family income and reducing the overall tax burden. Pensioners (who are senior citizens) benefit from preferential interest rates also, typically 0.5% to 0.75% higher than standard rates.

- Significant Tax Advantages

While pension income is fully taxable, the commuted amount is entirely tax-free. Crucially, the portion of pension foregone towards commutation recovery is also completely exempt from tax. Without commutation, the same amount would be taxed at the retiree’s marginal rate – often resulting in a tax outgo approaching one-third of the amount.

- Favourable Interest Dynamics

Although the implicit interest rate on commutation is 8% per annum, it is calculated on a simple interest basis. In contrast, returns on bank fixed deposits are compounded, usually quarterly. Over a 15-year period, simple interest at 8% per annum is equivalent to only 5.29% per annum compounded quarterly, making commutation financially advantageous.

Conclusion

Even after accounting for the flawed post-2008 commutation table, higher implicit interest, and a 15-year recovery period, pension commutation remains a sound financial decision for most government retirees – particularly those in moderate to higher tax brackets. It provides liquidity, tax efficiency, family security, and favourable long-term financial outcomes.

In sum, commuting your pension is not merely advisable – it is financially prudent.

Excellent advice and analysis by Shri JK Khanna, the well known successful warrior for the rights of of Pensioners and family pension holders. It’s is hoped that the 8CPC will take note of the facts and include in their recommendations – relief to the post-2008 retirees who opted for commutation of pension.